The Bank of England is expected to unveil the biggest interest rate rise in decades today.

A hike of 0.75 percentage points is anticipated – pushing the base rate to 3%, levels that have not been seen since 2008.

If confirmed, this could push up mortgage bills for millions of people in the coming months.

Supermarket offers 1p ready meals – cost of living latest

This would also be the eighth time in a row that the Bank of England has hiked interest rates. Less than a year ago, the base rate was just 0.1%.

Earlier this month, the markets had predicted that today’s increase could be one whole percentage point – but sentiment has calmed since the mini-budget was reversed and Liz Truss resigned as prime minister.

The Bank of England is also set to release long-term inflation forecasts, which are expected to show that the cost of living next year will be much higher than its target of 2%.

Official figures released in September showed inflation hit 10.1% – matching a 40-year high seen in July – with much of this increase driven by rising food costs.

Through these rate hikes, the Bank of England is trying to bring core inflation under control, which excludes more volatile elements such as petrol and energy prices.

Analysts at Deutsche Bank have warned they expect the BoE’s forecasts to show “the economic outlook has deteriorated further”, adding: “Conditioned on market pricing, the UK economy will likely fall into a deeper and more prolonged recession.”

Read more:

Heating off, buying food with credit cards – the impact of rising prices

Thousands too ashamed to go to work because they can’t afford soap

Low-cost grocery prices rocket – which ones have gone up most

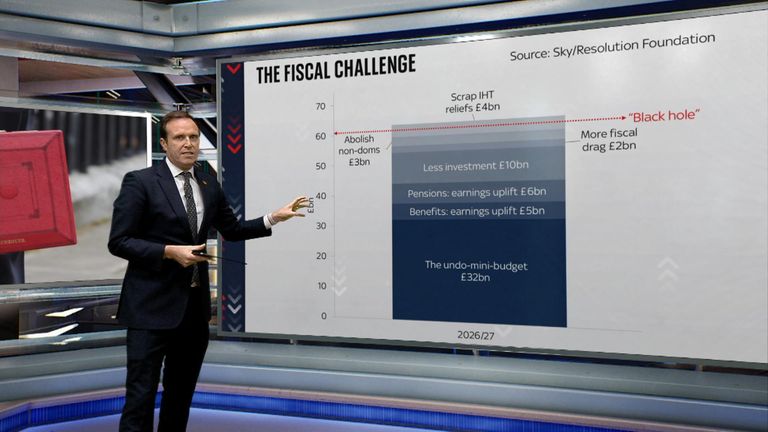

‘Black hole’ in finances explained

Firms face ‘desperately difficult decisions,’ Labour warns

This afternoon, Labour’s shadow chancellor will warn that the latest interest rate rise will have a huge impact on consumers and companies alike.

Speaking at the Anthropy conference in Cornwall, Rachel Reeves will say: “Rising interest rates will mean families with already stretched budgets will be hit by higher mortgage payments. It will mean higher financing costs for businesses.

“For many firms who have had a tough couple of years, this will mean desperately difficult decisions about whether to carry on.

“And it will mean profound implications for growth as demand is sucked out of the economy – and even those firms that are keeping their head above water face difficult decisions about whether to invest or expand.”

Yesterday, a new poll carried about by Ipsos for Sky News revealed that more than a quarter of people have started using their credit cards to buy food – and a fifth have borrowed money to adjust to rising prices this year.

Read more:

Almost half of adults finding it difficult to afford their bills

Tesco raises meal deal price for first time in a decade

The very real costs of having a premature baby

People putting food bills on credit

US also increases interest rates

The Bank of England’s decision will come a day after America’s central bank, the Federal Reserve, also confirmed that it will increase interest rates by 0.75 percentage points.

Wall Street fell sharply when Fed Chairman Jerome Powell suggested the US base rate may need to go even higher than previously thought to tackle the worst inflation seen in decades.

He warned: “It’s very premature, in my view, to think about or to be talking about pausing our rate hikes. We have a ways to go.”

Mr Powell also said that the Federal Reserve would rather make a mistake of taking interest rates too high than easing too quickly, amid fears that a premature pullback could cause inflation to remain.